UCO Bank Fraud Case study

The UCO Bank fraud illustrates how governance failure at the highest levels, when coupled with systemic technology vulnerabilities, can trigger large-scale financial loss and reputational damage.

This case combines ₹6,210.7 crore in loan diversion with ₹820 crore in cyber-triggered miscredits, revealing a dual-threat risk profile that every financial institution should treat as a high-priority scenario.

Case Background

| Key Parameter | Data |

|---|---|

| Institution | UCO Bank |

| Loan Diversion Amount | ₹6,210.7 crore |

| Cyber Miscredit Amount | ₹820 crore |

| Affected Accounts | ~41,000 (IMPS miscredits) |

| Recovery Achieved | ₹705.3 crore (~86% of cyber loss) |

| Primary Causes | Leadership misconduct, IT control lapses |

Fraud Mechanism – Loan Diversion

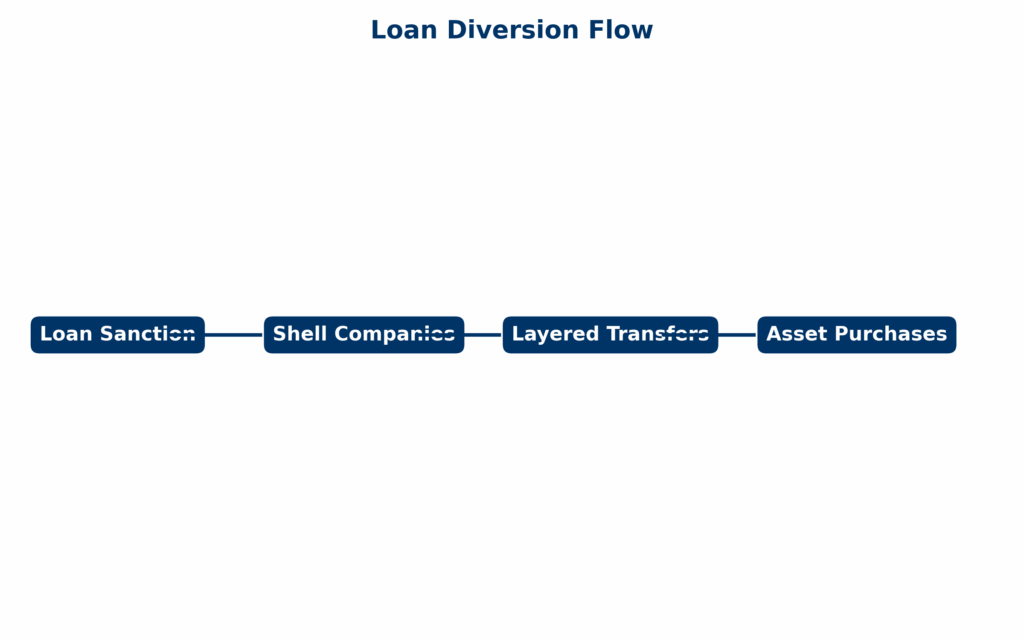

In the UCO Bank case, one of the core mechanisms identified was loan diversion. Large corporate exposures were approved despite clear adverse credit indicators—suggesting either a severe lapse in due diligence or deliberate negligence. Once sanctioned, the funds were systematically routed through a network of shell entities, enabling complex layering that effectively obscured the transaction trails. This diversion was not merely for operational misuse; evidence points to personal enrichment by key individuals, including the acquisition of high-value assets and acceptance of non-monetary inducements. GAFA’s analysis flags this as a textbook example of how inadequate credit risk governance, when paired with deliberate obfuscation tactics, can convert legitimate lending into a well-disguised vehicle for financial crime.

Fraud Mechanism – IMPS Miscredit Incident

Another striking element of the UCO Bank case was the IMPS miscredit incident, where the bank’s Immediate Payment Service (IMPS) system was allegedly exploited to transfer substantial sums into unintended accounts. The manipulation appears to have involved both technical vulnerabilities and possible insider collusion, enabling rapid, high-value transfers without triggering standard reconciliation alerts. Once miscredited, the funds were quickly dispersed or withdrawn, making recovery difficult. GAFA’s assessment underscores that while IMPS is designed for speed and efficiency, inadequate transaction monitoring and weak exception handling protocols can turn it into a high-speed channel for fund siphoning—especially when coupled with human complicity.

GAFA’s Analytical Insights

- Governance Breakdown

Leadership override of credit risk frameworks indicates structural weaknesses in board oversight and audit independence. - Technology Vulnerability

Single-point configuration changes without layered authentication enabled large-scale unauthorized credits. - Control Gaps

Delayed anomaly detection allowed fraudulent withdrawals before containment measures began. - Risk Interconnectivity

The simultaneous occurrence of governance and cyber failures magnifies operational risk beyond conventional fraud scenarios.

GAFA’s Recommendations

- Integrated Governance and Cyber Oversight-Financial crime doesn’t care about an organisation’s internal silos. To stay ahead, banks need oversight that brings together operational checks, IT security, and credit risk management into a single, coordinated framework.

- Mandatory Forensic Audits for Big Loans-Any loan above a set high-value threshold should be subject to both digital and financial forensic audits—before it’s approved and again after the money is disbursed. This ensures red flags are caught early and misuse is traced quickly.

- Predictive Fraud Analytics-It’s time to move beyond basic rule-based alerts. AI-driven systems that can spot unusual patterns before they become fraud give banks a real chance to stop crimes in motion, rather than cleaning up after the damage is done.

Conclusion

The UCO Bank case is not simply a matter of poor leadership or a tech “glitch.” It is a demonstration of compound risk—where governance lapses create fertile ground for cyber vulnerabilities to be exploited.

GAFA views this as a definitive case study on why integrated fraud prevention strategies must be at the core of financial institution risk policy.