In today’s increasingly regulated financial ecosystem, compliance is no longer optional it’s a strategic necessity. Financial institutions face growing scrutiny from regulators, and one of the most critical components of compliance is implementing a strong AML risk assessment framework.

A well-defined AML risk assessment doesn’t just help institutions stay compliant—it protects them from financial crime, reputational damage, and regulatory penalties. Yet, many organizations struggle with structuring an effective approach.

This guide walks you through a step-by-step AML risk assessment framework that is practical, scalable, and aligned with regulatory expectations.

What is an AML Risk Assessment Framework?

An AML risk assessment framework is a structured methodology used by financial institutions to identify, evaluate, and mitigate risks related to money laundering and terrorist financing.

It helps organizations answer key questions:

- Where are we most vulnerable?

- What types of customers or transactions pose higher risk?

- How strong are our current controls?

Rather than treating compliance as a checkbox activity, this framework enables a risk-based approach, which is now a global regulatory standard.

Enroll the AML Certification

Why AML Risk Assessment is Critical for Financial Institutions

Ignoring AML risks can lead to heavy penalties and long-term damage. Regulators expect institutions to proactively assess and manage risks.

Key benefits of implementing an AML risk assessment framework include:

- Improved regulatory compliance

- Early detection of suspicious activities

- Better allocation of compliance resources

- Stronger internal controls and governance

- Protection against financial and reputational loss

In essence, a structured AML framework transforms compliance from reactive to proactive.

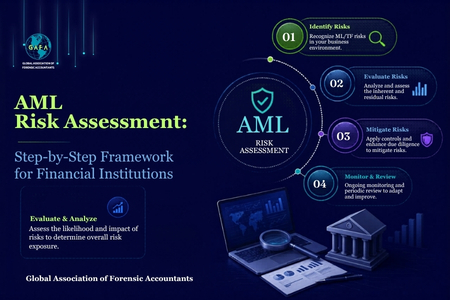

Step-by-Step AML Risk Assessment Framework

Below is a proven step-by-step AML risk assessment framework that financial institutions can adopt.

Step 1: Identify Risk Categories

The first step is to define the key risk areas relevant to your institution. Typically, AML risks fall into four main categories:

- Customer Risk – Type of clients (individuals, corporates, PEPs)

- Geographic Risk – Countries with high corruption or weak AML laws

- Product & Service Risk – High-risk offerings like cross-border transfers

- Transaction Risk – Unusual patterns or large-value movements

A strong AML risk assessment framework begins with clearly mapping these risk dimensions.

Step 2: Collect Relevant Data

Once risks are identified, the next step is gathering data to evaluate them.

This includes:

- Customer profiles and KYC data

- Transaction history and patterns

- Geographic exposure reports

- Product usage insights

The quality of your AML risk assessment framework depends heavily on data accuracy. Incomplete or outdated data can lead to flawed risk evaluations.

Step 3: Assign Risk Scores

After collecting data, assign risk ratings to each category. Most institutions use a scoring model such as:

- Low Risk

- Medium Risk

- High Risk

You can also use numerical scoring (e.g., 1–5 scale) to make the assessment more granular.

For example:

- A politically exposed person (PEP) may score higher under customer risk

- Transactions involving high-risk jurisdictions may score higher under geographic risk

This scoring system forms the backbone of your AML risk assessment framework.

Step 4: Evaluate Existing Controls

An AML risk assessment is incomplete without reviewing the effectiveness of current controls.

Assess:

- KYC and customer due diligence processes

- Transaction monitoring systems

- Suspicious activity reporting (SAR) mechanisms

- Internal policies and training programs

The goal is to identify gaps between existing controls and potential risks.

Step 5: Calculate Residual Risk

Residual risk is the level of risk remaining after applying controls.

Formulaically, it can be understood as:

Residual Risk = Inherent Risk – Control Effectiveness

This step helps financial institutions understand whether their controls are sufficient or need strengthening.

A mature AML risk assessment framework focuses heavily on managing residual risk, not just identifying inherent risk.

Step 6: Document the Assessment

Documentation is crucial for both internal governance and regulatory audits.

Ensure your AML risk assessment framework includes:

- Risk methodology

- Scoring criteria

- Data sources

- Findings and conclusions

- Action plans

Regulators often review documentation to assess how well your institution understands its risk exposure.

Step 7: Implement Risk Mitigation Measures

Based on your findings, implement targeted mitigation strategies.

Examples include:

- Enhanced Due Diligence (EDD) for high-risk customers

- Strengthening transaction monitoring rules

- Restricting services in high-risk jurisdictions

- Increasing frequency of risk reviews

Your AML risk assessment framework should always lead to actionable outcomes—not just reports.

Step 8: Continuous Monitoring and Review

AML risk assessment is not a one-time exercise. Risks evolve, and so should your framework.

Best practices include:

- Periodic reassessment (quarterly or annually)

- Real-time monitoring of high-risk transactions

- Updating risk models based on new regulations

- Incorporating emerging threats

Continuous monitoring ensures your AML risk assessment framework remains effective and relevant.

Learn more about the AML Certification

Common Challenges in AML Risk Assessment

Even with a structured approach, financial institutions often face challenges such as:

- Poor data quality or siloed systems

- Over-reliance on manual processes

- Lack of skilled compliance professionals

- Difficulty in quantifying risk

- Rapidly changing regulatory requirements

Addressing these challenges requires a combination of technology, training, and strategic planning.

Best Practices for an Effective AML Risk Assessment Framework

To build a robust AML framework, consider these best practices:

- Adopt a risk-based approach rather than a one-size-fits-all model

- Leverage automation tools for data analysis and monitoring

- Ensure cross-department collaboration between compliance, risk, and operations

- Maintain clear documentation and audit trails

- Regularly train employees on AML compliance

A well-implemented AML risk assessment framework not only ensures compliance but also enhances operational efficiency.

The Role of Technology in AML Risk Assessment

Modern financial institutions are increasingly using technology to strengthen their AML efforts.

Key technologies include:

- AI-powered transaction monitoring

- Machine learning for anomaly detection

- Automated risk scoring systems

- Data analytics platforms

These tools help reduce manual errors, improve accuracy, and scale your AML risk assessment framework effectively.

Conclusion

An effective AML risk assessment framework is the cornerstone of a strong compliance program. It enables financial institutions to identify vulnerabilities, implement controls, and stay aligned with regulatory expectations.

By following a structured, step-by-step approach—combined with continuous monitoring and technological support—organizations can not only mitigate risks but also build long-term trust and credibility in the financial ecosystem.

FAQs

Q1. What is an AML risk assessment framework?

Answer: An AML risk assessment framework is a structured process used by financial institutions to identify, evaluate, and mitigate risks related to money laundering and terrorist financing. It involves analyzing customer profiles, transactions, geographic exposure, and product risks. This framework helps organizations adopt a risk-based approach, ensuring compliance with regulatory requirements while improving operational efficiency and minimizing exposure to financial crimes.

Q2. How often should AML risk assessments be conducted?

Answer: AML risk assessments should ideally be conducted annually, but high-risk institutions may require more frequent reviews. Additionally, assessments should be updated whenever there are significant changes such as new products, expansion into new markets, or regulatory updates. Continuous monitoring is also essential to ensure the AML risk assessment framework remains relevant and effective against evolving financial crime threats.

Q3. What are the key components of an AML risk assessment?

Answer: The key components include risk identification, data collection, risk scoring, evaluation of controls, residual risk calculation, documentation, and continuous monitoring. These elements work together to provide a comprehensive understanding of an institution’s risk exposure. A well-defined AML risk assessment framework ensures that each component is aligned with regulatory expectations and organizational goals.

Q4. Why is a risk-based approach important in AML?

Answer: A risk-based approach allows financial institutions to focus their resources on high-risk areas rather than applying uniform controls across all operations. This improves efficiency and ensures better detection of suspicious activities. Regulators worldwide emphasize this approach as it enhances the effectiveness of an AML risk assessment framework while reducing unnecessary compliance burdens.

Q5. How can technology improve AML risk assessment?

Answer: Technology enhances AML risk assessment by automating data analysis, improving accuracy, and enabling real-time monitoring. Tools like AI and machine learning can detect unusual patterns and assign risk scores more efficiently than manual processes. Integrating technology into an AML risk assessment framework helps institutions scale their compliance efforts and respond quickly to emerging risks.